How to Actually Build Wealth and Retire Early (Explained in 6 Minutes)

How Ordinary People Build Extraordinary Wealth

I started investing 20+ years ago with $1,000 while I was still in school.

That portfolio now makes enough money for me to live off.

I’ve watched people make huge returns during this time. I’ve also watched people lose everything.

This isn’t a get rich quick guide. It’s how to build wealth safely over the long term.

A quick note: All the numbers and returns in this article are general assumptions based on historical averages. Your actual results will vary. This isn’t financial advice, just what I’ve learned and what has worked for me.

The Most Important Thing That You Need to Understand

You cannot get rich on a salary alone.

It doesn’t matter if you make $50,000 or $500,000 per year because trading your time for money has a limit.

Wealth comes from owning things that make money while you sleep. The best option is owning a business you control, where you make the decisions, hire the team, keep all the profits, and build something worth millions over time. The second option is owning businesses that other people run, where you don’t pick the strategy or manage the team but you own a piece of the profits.

Most people will never start or buy a business, but you can still become an owner by owning small pieces of many businesses instead of one big piece of one business. This is what the stock market actually is. When you buy an index fund, you own tiny pieces of thousands of companies.

The strategy is simple: become an owner, spread your money across many companies so you can’t pick wrong, and wait long enough for your ownership to grow in value.

Before we go further: If you already have another vehicle that gives you ownership, liquidity, growth, and diversification based on a proven financial system like index funds, then you probably don’t need this guide. If you’re running your own business, investing in private equity, or you’re a real estate mogul with lots of access to capital, then more power to you. This guide is for everyone else who needs a simple, reliable path to financial freedom.

1. Why Owning Beats Working

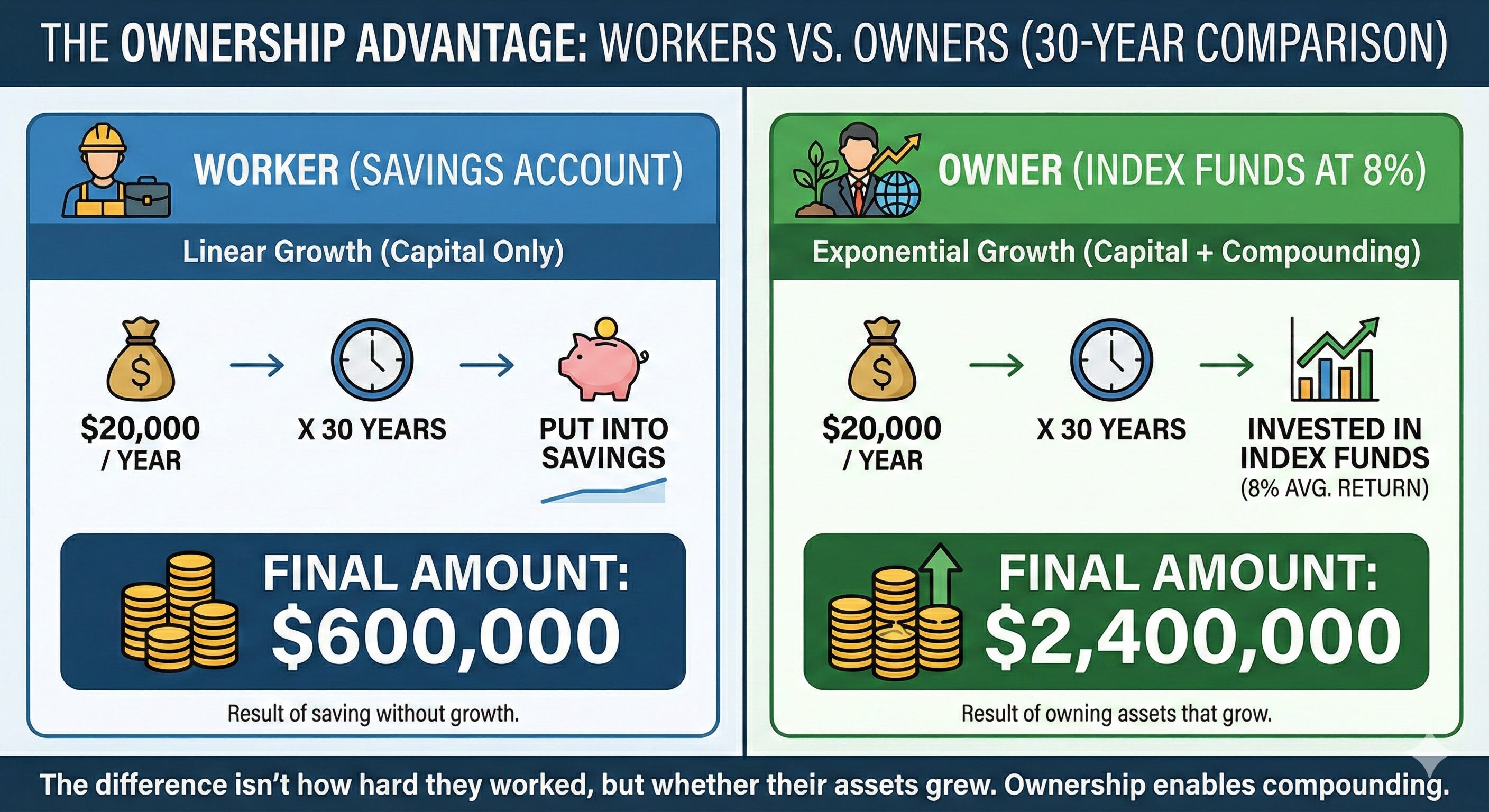

Most people work hard, get a raise, save some money, and put it in a savings account, then retire at 65 with maybe $500,000 if they’re lucky. Owners buy pieces of businesses that grow over time, which means the value of their ownership grows too, and they retire at 50 with $3 million.

The difference isn’t how hard they worked but whether they owned assets that grew.

Say you earn $100,000 per year and save 20%, which means you’re putting away $20,000 per year. After 30 years, you have $600,000 saved.

Now take that same $20,000 per year and buy ownership in businesses that grow at 8% every year. After 30 years you have $2.4 million because owners capture growth while workers capture wages, and growth builds on itself while wages don’t.

2. How to Become an Owner Without Starting a Business

The easiest way to become an owner is buying index funds, which are collections of many companies packaged together.

For first-time investors who want broad diversification, a good option is an all-world fund, where one purchase gives you ownership in the whole global stock market including Apple, Microsoft, Toyota, Samsung, and 3,000 other companies.

When you own as many businesses as possible, you capture the growth of the whole economy, which means when any company wins, you win.

Here’s what I actually do: I use only two vehicles for investing. About 80% of my money buys the broad market through S&P 500 ETFs like VOO and SPY, and the other 20% goes into specific sectors I believe will do really well over the long term like technology, healthcare, and financials through ETFs like XLK, XLV, and XLF.

I don’t pick individual stocks and I don’t use complicated strategies.

I watched three friends try to pick winning stocks in 2021, and all three are down 40% or more while my boring index fund approach that owns everything is up 65%.

Professional investors with billion dollar budgets can’t beat the market, and fewer than 10% do it over 20 years. What I am trying to say is that the odds are you are not going to beat the market by trading hot stocks.

Even if you could pick winners, taxes would destroy your gains because every time you sell a stock, you pay taxes. When you buy and hold for decades, you delay paying taxes and your money grows faster because the government isn’t taking a cut every year.

Remember, trying to pick stocks and trading them a lot will cost you 20% to 37% of your gains in taxes every single year… and as you may have guessed, taxes are the biggest drag on wealth creation.

3. Why Time Matters More Than Timing

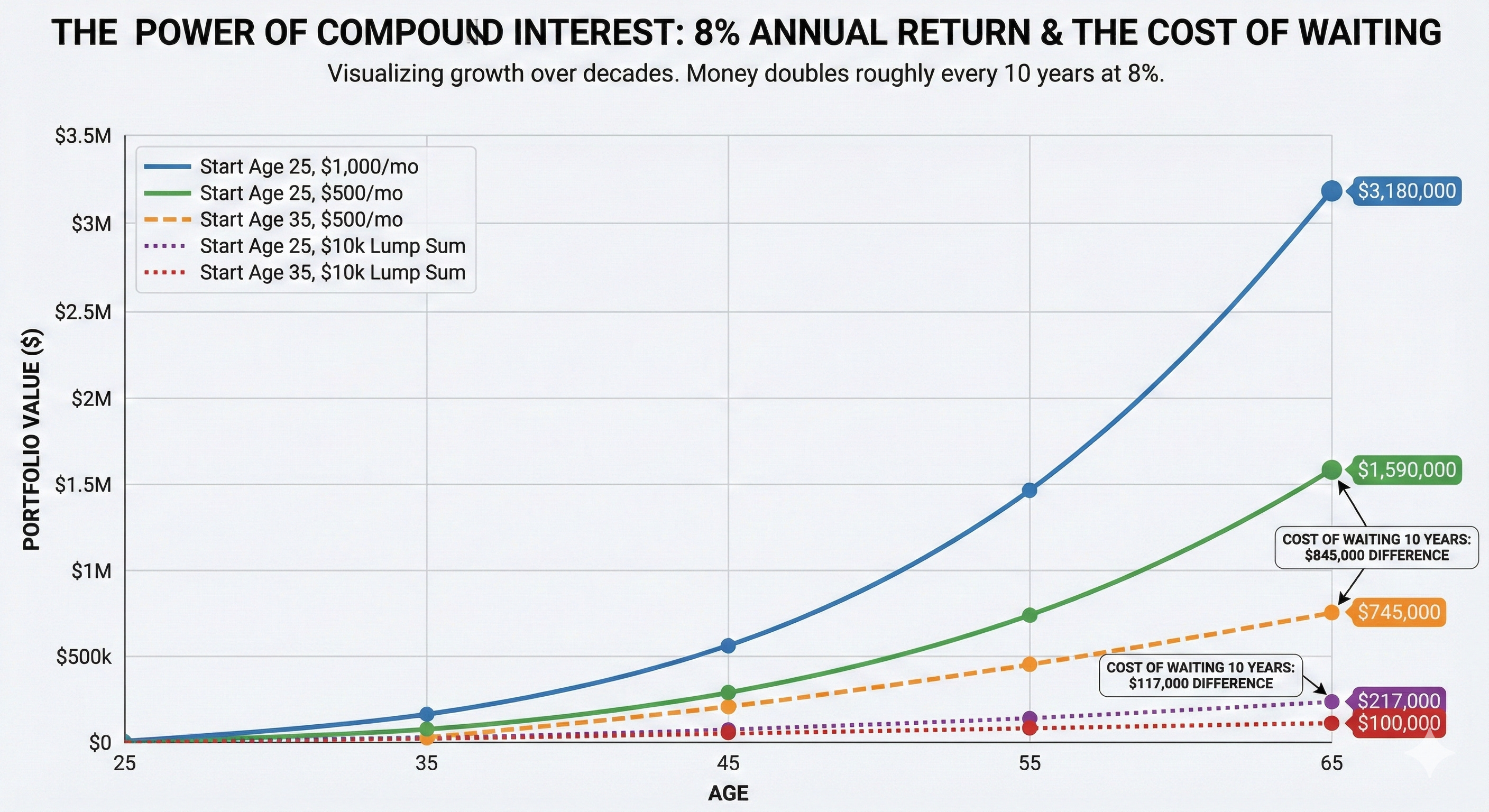

An 8% return every year doesn’t sound impressive until you understand how it builds on itself.

The money you make starts making money, then the money that money made starts making money, and this cycle repeats for decades. Your money roughly doubles every 10 years at 8% returns.

Say you put in $10,000 at age 25 and you’ll have $217,000 at age 65 without adding another dollar. If you wait until age 35 to start, you only get $100,000. Waiting one decade costs you $117,000.

Start at 25, invest $500 per month:

Age 65: $1,590,000

Start at 35, invest $500 per month:

Age 65: $745,000

Same monthly amount and same discipline, but the difference in when you started costs you $845,000.

Start at 25, invest $1,000 per month:

Age 65: $3,180,000

When you double your monthly investment, you more than double the result because time does most of the work.

4. Why You Should Start Today?

Start now and don’t wait for the perfect time because your goal is to own businesses for as long as possible.

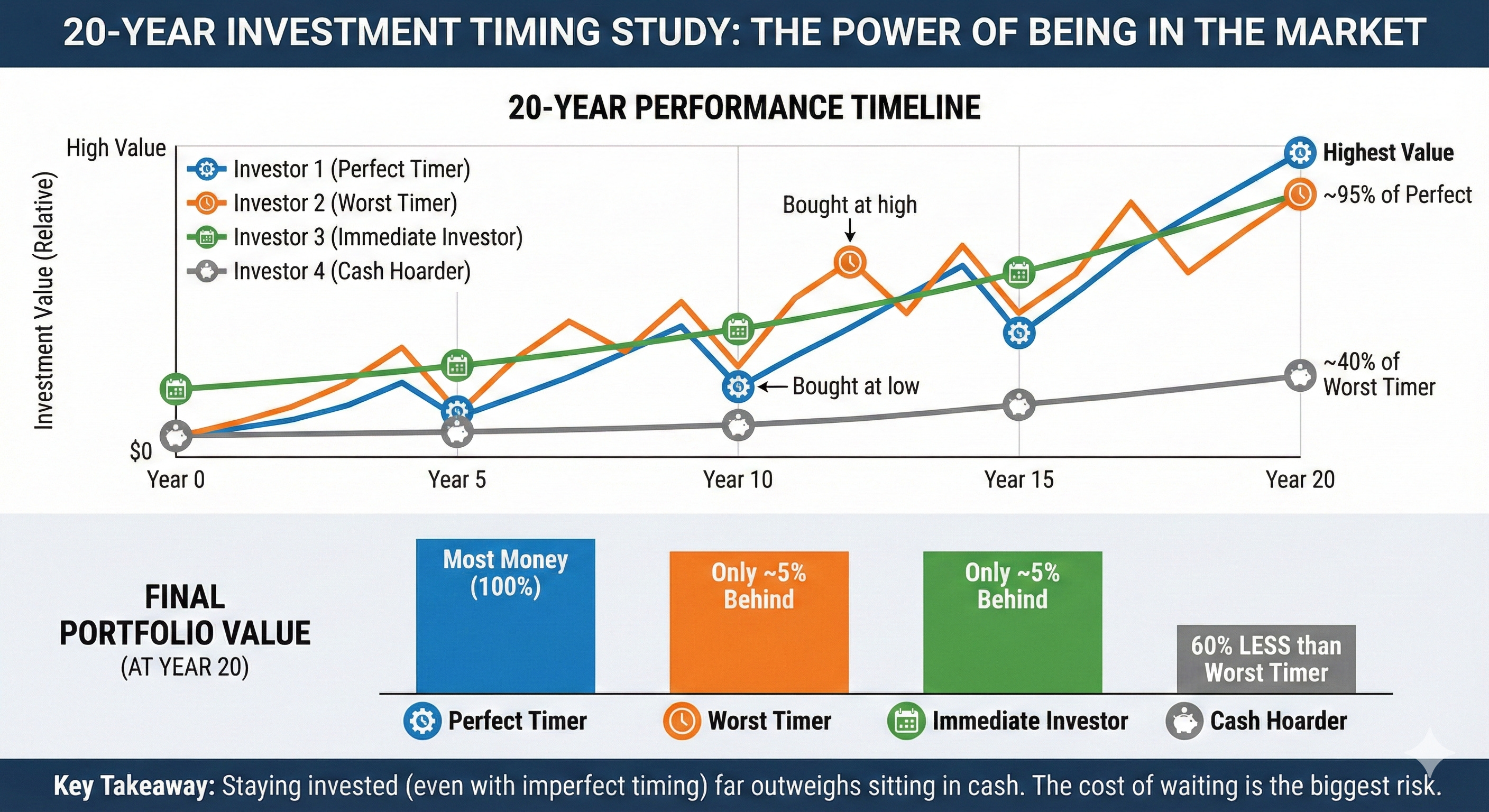

A study looked at four different investors over 20 years:

Investor 1: Had perfect timing and only bought at the absolute lowest point each year

Investor 2: Had the worst timing and only bought at the absolute highest point each year

Investor 3: Invested immediately and put in all their money on January 1st each year

Investor 4: Stayed in cash and kept their money in savings waiting for the right time

After 20 years, the perfect timer made the most money, but the worst timer and the immediate investor were only 5% behind. All three crushed the person who sat in cash, who had 60% less money than even the worst timer.

The 10 best trading days account for most of the gains in any given year. If you’re sitting in cash trying to time your entry, you’ll probably miss these days. Research shows that missing just the 10 best days over 20 years cuts your returns in half, and missing the 20 best days cuts your returns by 75%. You can’t predict when these days will happen because they often come right after the worst days when everyone is scared.

People who waited from January 2020 until things calmed down missed a 60% gain. History shows that almost every previous all-time high looks ultra-cheap years later.

I bought my first index fund the week I got my first real paycheck, not because prices looked good (I had no idea about anything, I just bought the market) but because waiting for the right time is how you end up 55 years old with nothing.

5. What Else Should You Own?

Here is my simple take when you are starting out: Index funds should be 70% to 80% of your money at minimum.

My friend put 60% of his money into rental properties in 2019, and he spent 200 hours dealing with tenants last year while his return was 4%.

My index funds returned 12% and took zero phone calls.

Crypto makes little sense for most people, with Bitcoin being the only exception. Buy small. If you don’t know anything about crypto and want some exposure, you can use my strategy of keeping it to 2% to 4% of your portfolio once you have real money invested. But if you know a lot about crypto and you’re actively involved, then maybe you could take a bigger sized bet.

I bought some Bitcoin for each of my kids, not as a main part of my plan but as a lottery ticket. If Bitcoin explodes, my kids win, and if it doesn’t, we’re not counting on that money anyway.

Real estate is complicated and depends on where you live. I only started becoming a real estate investor in the last 15 years, and real estate is now my number one asset class where I own more than 3,500 units.

But all the money I made before real estate is what allowed me to buy real estate in the first place.

Buying property makes sense when you already have a large portfolio and want to spread your money around more, or when you’re willing to spend a lot of time and really understand your local market or the asset class. Otherwise you won’t beat stock market returns and you’ll have much more work.

My allocation guideline:

This is just what I’ve seen and learned from different friends. You’re welcome to play around with it or use this as a starting point.

Under $100,000: 100% index funds (start with something simple like VOO)

$100,000 to $500,000: 75% broad market index funds, 20% sector ETFs if you want, 5% Bitcoin if you want

Over $500,000: 70% index funds, spread the rest based on your situation

I prefer to spend my time working on things that I can control so I try and keep my investing world as simple and efficient as possible. Spreading your money around costs time and makes things complicated, so it only helps when you have a lot of money.

6. When Can You Stop Working?

If there was any question that most people start thinking about as they get older it is, “When can I stop working?”

I wish there was a required course about this in high school or college but instead you have to read my post about this!

In an nutshell, returns don’t shake out evenly every year, which means market crashes force you to sell more ownership to pay the same bills. Over time this can shrink your portfolio even if your average return stays at 8%.

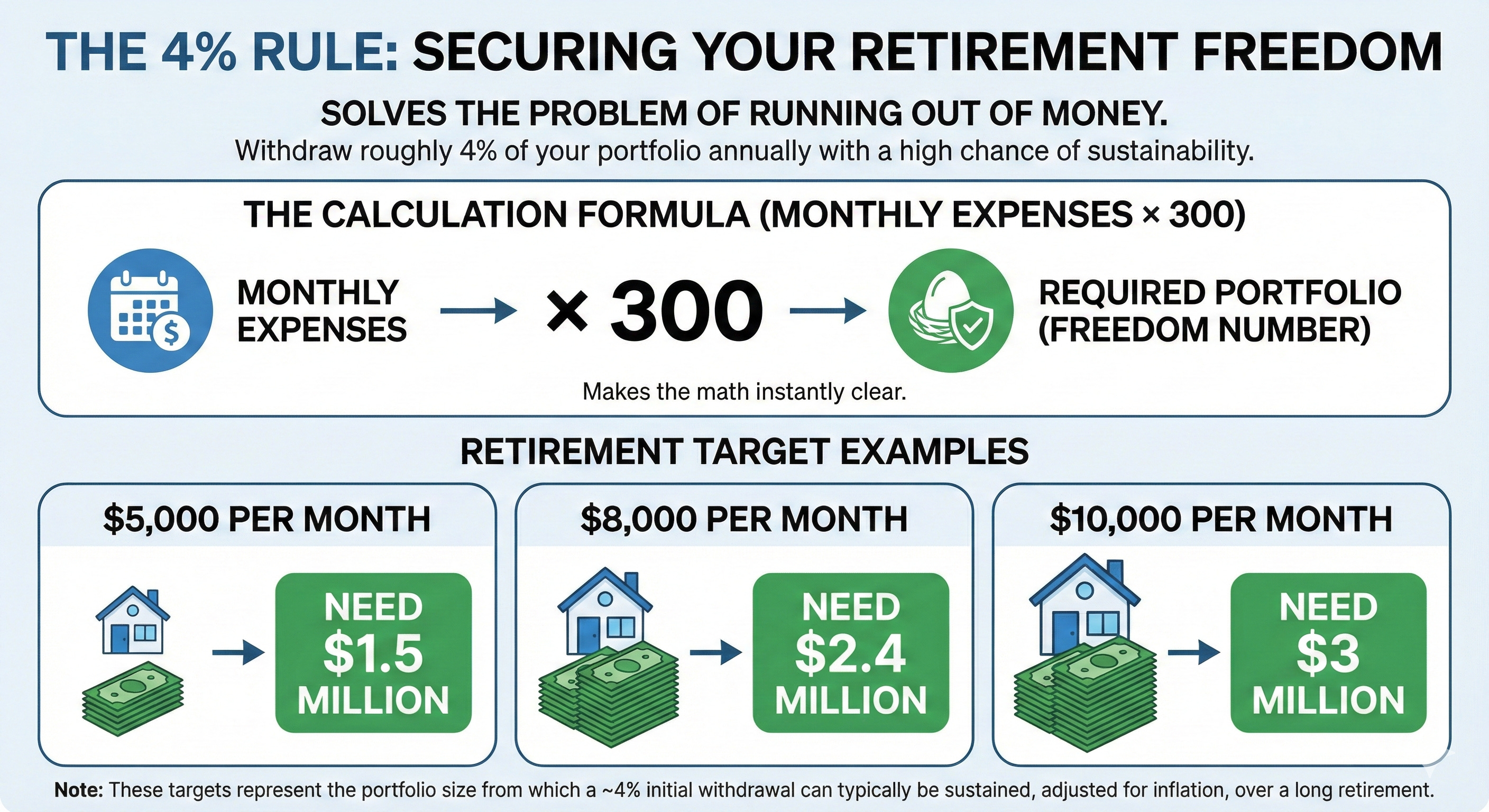

The 4% rule solves this problem. Meaning, you can take out roughly 4% of your portfolio each year with a high chance of never running out of money.

To calculate this number, just take your monthly expenses and multiply it by 300 to figure out how much you need.

Retirement targets:

$5,000 per month: Need $1.5 million

$8,000 per month: Need $2.4 million

$10,000 per month: Need $3 million

Pretty nifty.

Then just work backwards from there.

If you need $1.5 million and you’re 25 years old, putting in $1,000 per month at 8% gets you to $3.5 million in 40 years, while putting in $500 per month gets you to $1.75 million. If you’re 35 and need $1.5 million in 30 years, you need to invest $1,100 per month to hit that number.

Starting as early as possible matters more than any other decision because even small amounts make a huge difference over decades due to the power of compounding.

Bottom line:

Own your own business (or)

Own a piece of someone else’s business (stocks or private equity)

If you liked this post, then you’ll like this one too:

Thus so much useful i got to actually learn about the real life skill

As knew about info from everywhere but was real , expert result, best guide on ground reality

While being free of cost

Solid advice.